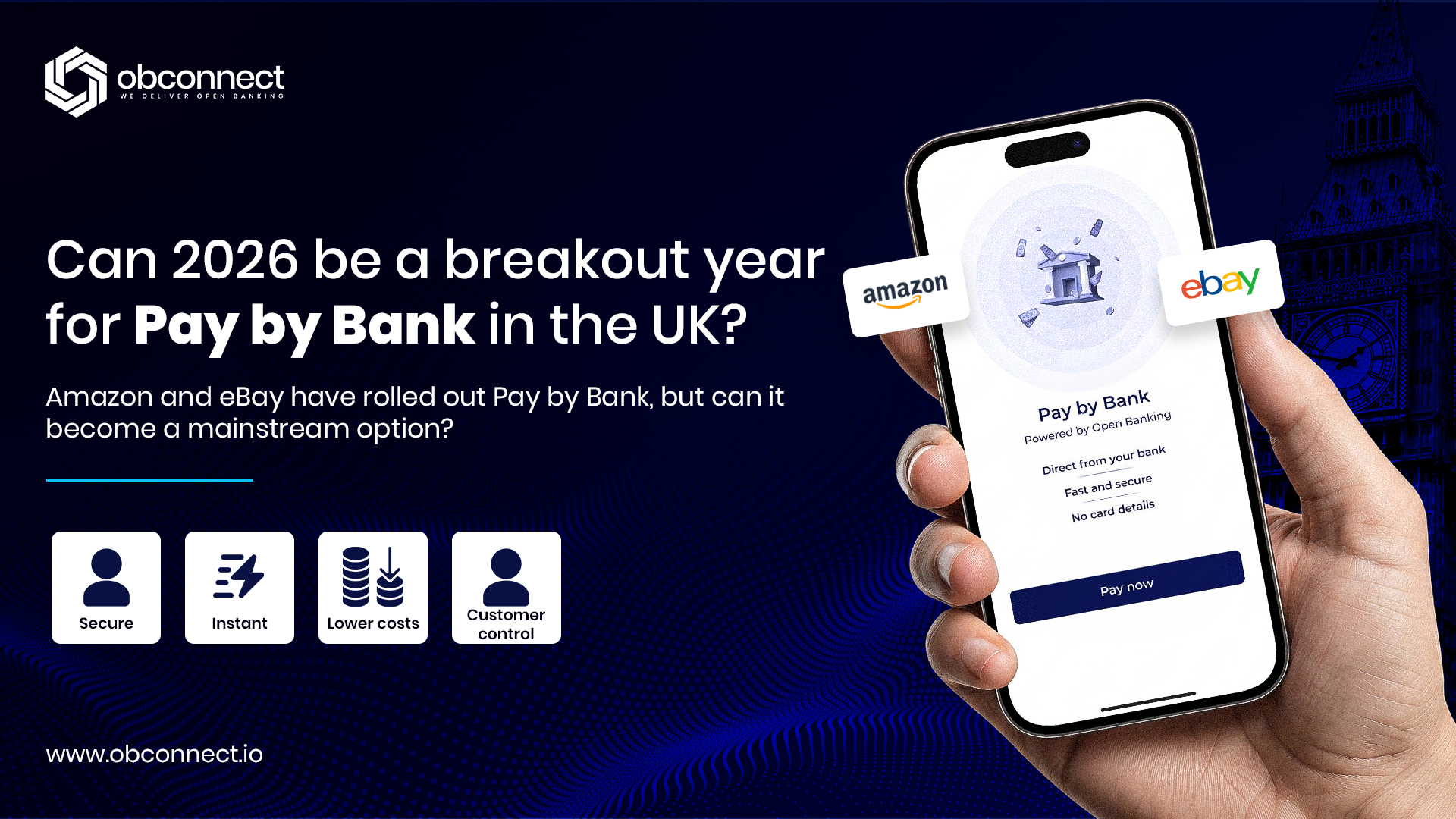

For years, Pay by Bank has been “on the brink”.

Talk to anyone in payments and you will hear the same sentiment. The technology is there. The benefits are obvious. The infrastructure works. And yet, it has consistently sat just outside the mainstream – promising, but not quite familiar behaviour.

That may finally be about to change. Because 2026 feels different.

Not because of a new regulation. Not because of a major technical breakthrough. But because of something far more powerful: exposure at scale.

The Moment Pay by Bank Enters the Real World

When global platforms like Amazon and eBay begin rolling out Pay by Bank at checkout, this is no longer an industry conversation. It becomes a consumer one.

For the first time, millions of people are not just hearing about Pay by Bank – they are seeing it. Sitting alongside cards. Presented as a viable, everyday option. And this is where adoption truly begins.

Historically, Pay by Bank has performed well in specific use cases. Tax payments. Airline bookings. Gaming. Environments where the user is perhaps more tolerant of trying something new, or where the value exchange feels more controlled.

But everyday retail? That has always been the hardest nut to crack. Cards are not just a payment method in retail – they are a habit. And habits are incredibly difficult to break.

Why This Time Might Be Different

The difference now is not the technology. It is the context.

Consumers are not being asked to seek out Pay by Bank. It is being placed directly in front of them, at the exact moment a payment decision is made.

That subtle shift matters more than any feature ever could.

We have seen this before. Payment adoption is rarely driven by capability alone. It is driven by visibility, repetition, and trust – the same principles that underpinned the success of Chip and PIN adoption in the early 2000s .

Back then, the technology worked well before consumers widely adopted it. What changed was not the product – it was the environment around it. Pay by Bank is now entering that same phase.

The Merchant Case Has Already Been Won

While the industry often focuses on consumer adoption, the reality is that merchants have understood the value of Pay by Bank for some time. And the reasons are hard to ignore.

Card payments come with layers of cost – interchange, scheme fees, acquirer fees – all of which eat into margins. Add fraud risk and operational complexity, and the picture becomes even clearer.

Pay by Bank simplifies this.

By leveraging Open Banking APIs and the UK’s Faster Payments infrastructure, merchants can receive funds directly, often faster, and with fewer intermediaries involved.

This is not just about saving money. It is about improving cash flow, reducing risk, and simplifying operations.

As we have explored in our Open Banking Challenge Series, cost and operational friction have historically been key barriers – but they are also the clearest opportunities .

From a merchant perspective, the question is no longer why adopt Pay by Bank? It is,when will consumers follow?

The Real Challenge: Behaviour, Not Technology

This is where 2026 becomes so important.

Because the success of Pay by Bank is no longer dependent on infrastructure.

The rails work. The regulation exists. The ecosystem is mature.

Open Banking has already demonstrated its ability to deliver secure, controlled, and transparent payment experiences – giving consumers direct visibility and control over their transactions .

But none of that guarantees adoption. Consumers do not change behaviour because something is better. They change behaviour because something feels normal.

The Power of Normalisation

This is why Amazon’s role cannot be overstated. When a consumer sees Pay by Bank once, it is an option. When they see it repeatedly, across multiple purchases, it becomes familiar. And when familiarity sets in, resistance begins to fade.

Add to that tangible benefits – such as faster refunds, potentially within minutes of a return being verified – and the value becomes not just theoretical, but real.

This is where Pay by Bank starts to compete not just on cost or security, but on experience. And experience is what drives habit.

What Happens If It Works?

If Amazon, eBay, and subscription ecosystems like Prime successfully normalise Pay by Bank, the impact could be significant.

We move from an “alternative payment method” to a “standard checkout option”. And eventually, to something even simpler: just payment.

At that point, the conversation changes entirely. We stop asking whether Pay by Bank will replace cards. Instead, we start asking where cards still make sense.

And If It Doesn’t?

It is equally important to recognise the other side of the equation.

If even this level of exposure cannot shift consumer behaviour, adoption may continue – but at a slower, more incremental pace.

Pay by Bank would remain strong in specific verticals, but struggle to fully break into everyday retail at scale.

That is why 2026 feels like a defining moment. Not for the technology – but for the mindset of the consumer.

Final Thoughts: A Year That Will Shape the Future of Payments

At obconnect, we have always believed that Open Banking payments are not a question of if, but when.

The industry has done the hard work. The infrastructure is in place. The value is clear.

What remains is the final piece of the puzzle: consumer trust, built through repeated, real-world use.

2026 is the year where that trust is tested at scale. And if it succeeds, Pay by Bank will no longer be positioned as the future of payments. It will simply become part of the present.

Ready to Be Part of the Shift?

At obconnect, we help businesses unlock the full potential of Pay by Bank – from reducing payment costs to delivering faster, more secure customer experiences.

If you are exploring how Open Banking can transform your payment strategy, get in touch with our team today.