Fraud is a global pandemic. We’ve all heard stories – from fake Facebook Marketplace listings to scam emails convincing staff to buy Apple gift cards “on behalf” of their boss. Fraudsters don’t follow a project plan or stick to the terms of reference. They act with agility, persistence, and creativity. It’s time we accept an uncomfortable truth: we will never completely eliminate fraud. Even in the most heavily regulated jurisdictions, it remains ever-present.

The problem intensifies when blame is disproportionately directed at banks. While banks are heavily regulated – and rightly so – to protect consumer funds, their adversaries face no such constraints. In many cases, fraud prevention remains reactive. That’s where we, at obconnect, stepped in.

Proactive fraud defence through Open Banking

From the early days of Open Banking, we recognised the wider potential of data-driven tools and regulatory APIs. We looked beyond narrow compliance use cases and focused on how data, when used at the right time, could not only prevent fraud but also reduce costly errors.

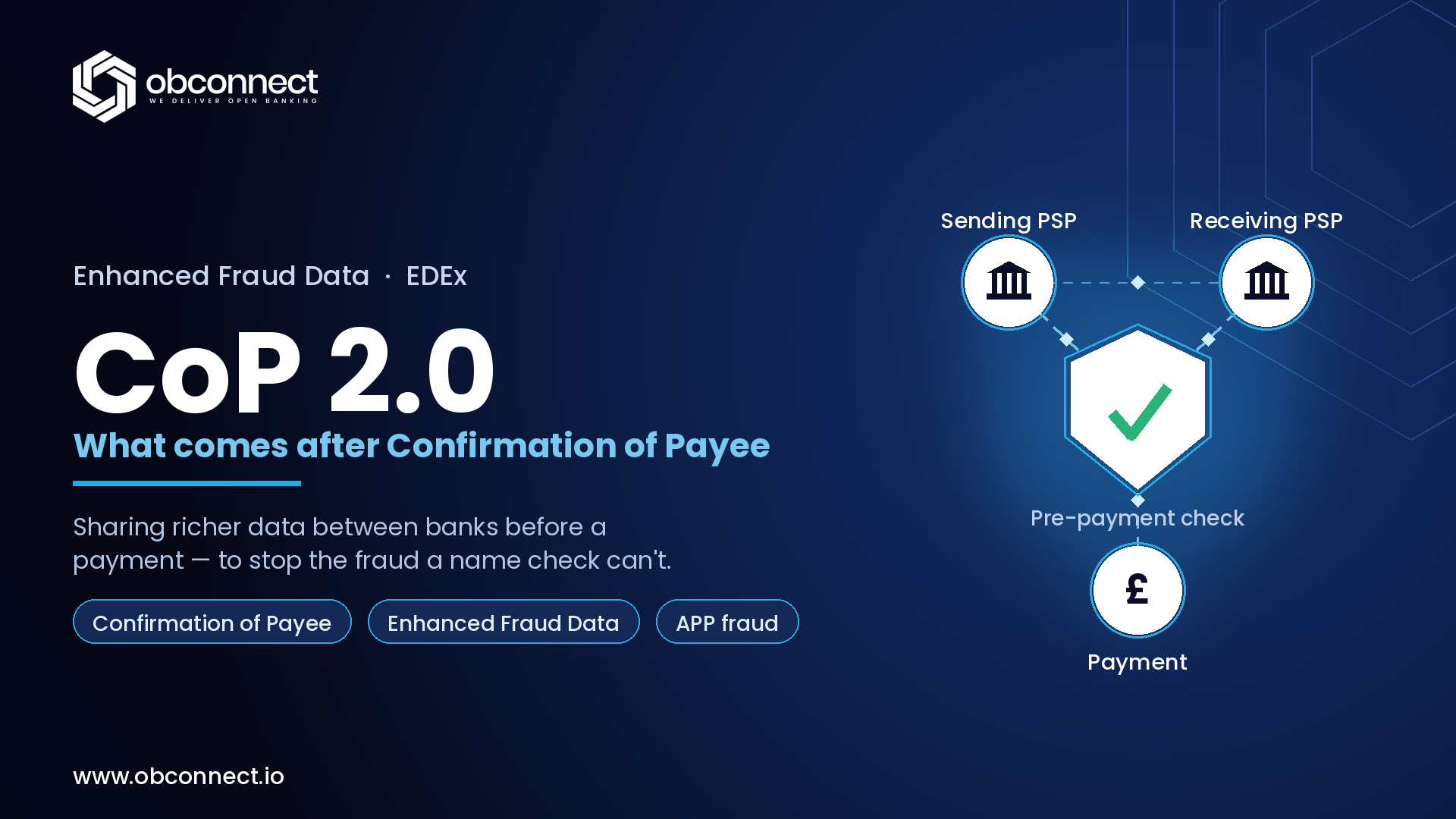

Confirmation of Payee (CoP) is a prime example. In the UK, CoP has become a foundational tool for fraud prevention – confirming account ownership before payments are made. This isn’t just useful for individuals; it supports salary payments, invoice validation, and identity checks, all of which help stop fraud in its tracks.

But the potential of CoP has always been restricted by regulatory narrowness. Fraud’s final act happens at the bank – but by then, it’s often too late. What’s needed is earlier intervention.

Measuring impact by observing fraudster behaviour

We can’t just count fraud losses to measure success. A telling indicator is how fraudsters respond. When they change tactics, we know we’re making a difference.

CoP is one such initiative that’s forced fraudsters to pivot. In the UK, it’s nearing maturity, thanks in no small part to Pay.UK’s open engagement with stakeholders across the fraud lifecycle. As a result, the UK is leading the charge in fraud prevention.

The rise of Verification of Payee across borders

Europe is following suit. Its own version of CoP – Verification of Payee (VoP) – benefits from being a second mover. Observing the UK’s rollout has helped European regulators understand what to encourage and what to avoid.

But there’s a critical point here: no fraud prevention tool is effective without reliable delivery. At obconnect, we’ve taken that to heart. Our solutions for CoP and Open Banking services are high-performing by design — dependable, responsive, and trusted by our partners. In fraud prevention, performance isn’t optional — it’s essential.

Lessons from New Zealand and the global opportunity

New Zealand has recently launched CoP with a uniquely open approach. Access isn’t limited to banks, and the service isn’t viewed as a singular product. They’re incorporating cross-border fraud data and testing international CoP interoperability – all from a shared, trusted-data framework. It’s a masterclass in forward-thinking strategy.

Looking ahead: The Facebook Marketplace test

Imagine a future where a Facebook Marketplace seller is required to verify their identity and their receiving account using CoP or VoP before listing an item. That’s the kind of world we should strive for – one where fraud is harder to commit at every step.At obconnect, we’ve seen first-hand that CoP and VoP offer far more than compliance tick-boxes. Their potential to make fraud harder to execute is real and tangible – but only if they’re implemented with the right strategy, technology, and vision.