The UK just launched its first new major payment scheme since 2008 — and most businesses have no idea

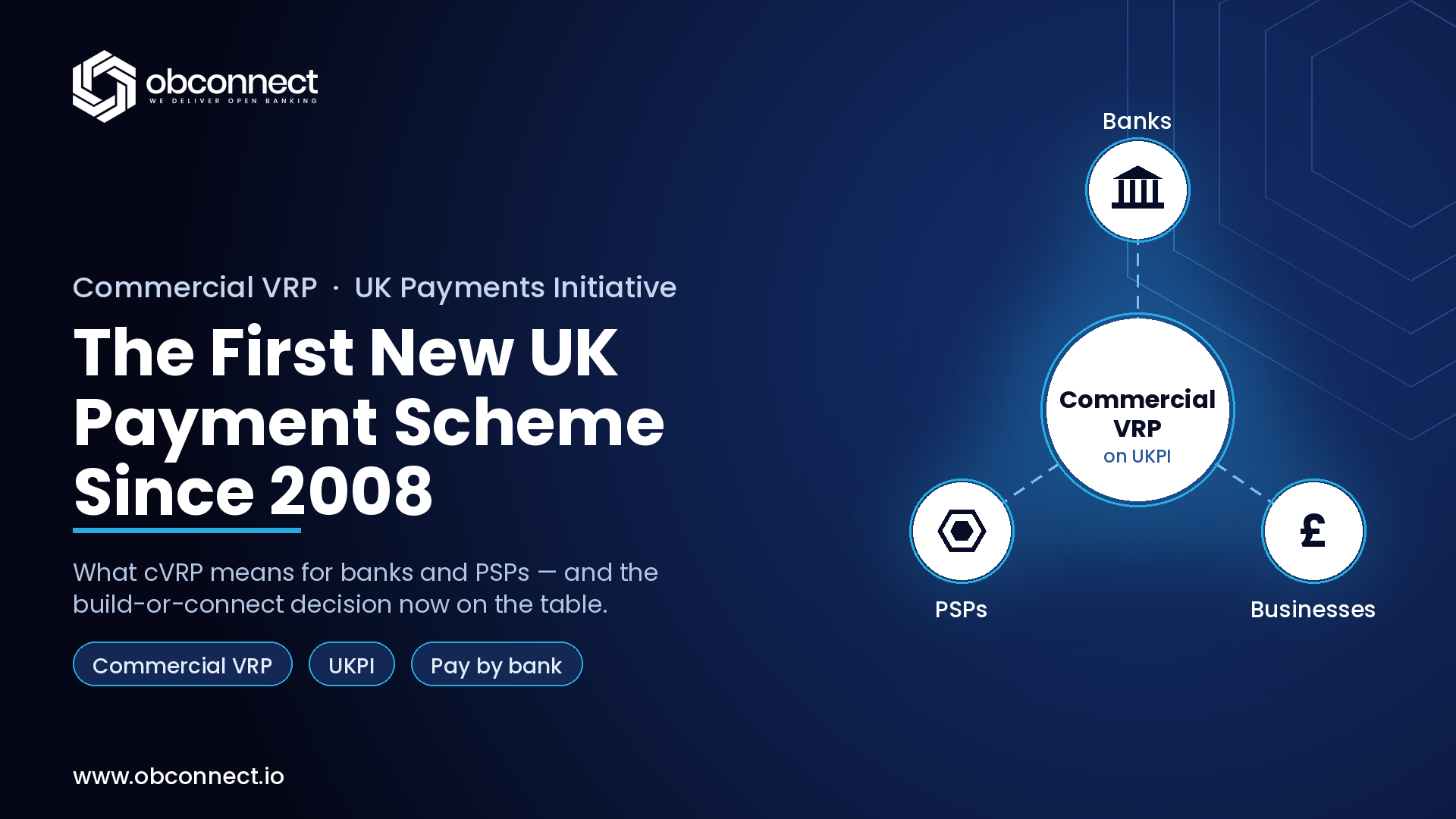

On 2 June 2026, the UK switched on its first new major payment scheme since Faster Payments in 2008. It’s called commercial Variable Recurring Payments – commercial VRP, or cVRP – and it’s operated through a new industry body, the UK Payments Initiative (UKPI). For most businesses it has passed almost unnoticed. For payments and product teams at banks and PSPs, it is one of the most consequential changes to the UK’s payments landscape in a generation.

This is a guide to what the cVRP scheme actually is, what the UKPI rulebook changes about scheme participation, settlement and the commercial model, and the build-or-connect decision now on the table.

First, the important distinction – cVRP is a scheme, not a product

It’s worth being precise, because the two get conflated constantly. A product is something a bank, fintech or merchant offers to customers – a savings account, Stripe Billing, a “Pay by Bank” checkout button. A scheme is the shared set of rules, standards, participant obligations and operating processes that let many different firms offer compatible products.

Visa, Mastercard, Bacs Direct Debit, CHAPS and Faster Payments are all payment schemes. cVRP is the same kind of thing. Through UKPI, the cVRP scheme defines how participants connect, the consent and authorisation rules, the liability and dispute processes, the commercial arrangements, and the technical standards. Banks and fintechs then build products on top of it:

- A utility’s “Pay by Bank Monthly” option is a product.

- A fintech’s recurring-payment API is a product.

- The underlying cVRP framework that makes those products possible and interoperable is the scheme.

Put simply: cVRP is a new UK payment scheme for recurring account-to-account payments, enabling banks and fintechs to build recurring-payment products on top of open banking rails. Get that distinction right and everything below falls into place.

What the cVRP scheme changes

Variable Recurring Payments already existed in a limited “sweeping” form: moving money between a customer’s own accounts (“me-to-me”). The cVRP scheme extends that framework so firms can build products that collect recurring payments from customers to pay real businesses — energy suppliers, government, charities and, in time, e-commerce — all under one set of rules.

For the end customer, products built on cVRP behave like a smarter, consent-driven alternative to Direct Debit and card-on-file: a long-lived, parameter-bound mandate (maximum amount, frequency, expiry), with payments initiated account-to-account over Faster Payments — near-instant, with the payer in control and strong customer authentication built in.

The reason it matters now isn’t the technology — VRP has been technically possible for some time. It’s that the scheme finally exists to make those products interoperable and commercially viable.

What the UKPI rulebook changes about scheme participation

Until now, anyone wanting to offer recurring A2A products at scale had to strike bilateral agreements bank by bank — slow, expensive and inconsistent. The cVRP scheme removes that.

UKPI is a new, industry-owned scheme established and funded by 31 founding organisations spanning both the demand and supply sides of payments — including Nationwide, NatWest Group, Mastercard Open Banking Services, GoCardless, TrueLayer, Yapily, Token.io, Moneyhub, Plaid, Acquired.com and obconnect. It provides a single rulebook, common operational standards and a shared commercial model, so every participant operates on the same terms.

For a payments or product team, that changes the participation question fundamentally:

- One rulebook, not many contracts. Connect to the scheme once, rather than negotiating with each bank individually.

- Defined roles. cVRP runs on the established open banking model — PISPs initiating payments and ASPSPs (the account-holding banks) exposing the rails — now governed by a single scheme rather than ad-hoc arrangements.

- Reach from day one. UKPI targeted around 75% of UK current accounts at Wave 1 launch, covering the major high-street banks — the threshold at which products built on the scheme become viable to offer customers.

What it changes about settlement and the commercial model

The headline shift is commercial. Instead of bespoke, bilateral economics negotiated institution by institution, the scheme introduces a shared, multilateral commercial model — a single arrangement under which participants are remunerated on standard terms. For the first time, recurring A2A payments have a sustainable commercial framework rather than a free-but-unfunded one, which is precisely what stalled earlier momentum.

Settlement itself remains account-to-account over existing real-time rails, so funds move with Faster Payments speed and finality. What’s new is the predictability: standardised scheme terms make the economics of building cVRP products modellable in advance, rather than a function of how hard each bilateral deal was fought.

Wave 1 now, Wave 2 next — who can build on it today

The scheme is rolling out in waves. Wave 1 (live now) covers regulated and trusted sectors:

- Energy, utilities and telecoms

- Regulated financial services

- E-money institutions

- Local and central government

- Registered charities

Wave 2 — general e-commerce — is expected in the second half of 2026. The sequencing is deliberate: start with lower-risk, recurring-bill use cases, then open up to broader retail. For banks and PSPs, Wave 1 is the window to get scheme participation, connectivity and propositions in place before the much larger e-commerce wave arrives.

The build-or-connect decision now on the table

To bring cVRP products to market, an institution can either build and maintain its own scheme-compliant capability — PISP/ASPSP connectivity, consent and mandate management, scheme conformance, ongoing rulebook upgrades — or connect through an existing scheme participant that already operates that infrastructure.

Building in-house means carrying the full cost of conformance and the ongoing burden of keeping pace with a rulebook that will evolve through Wave 2 and beyond. Connecting through a participant means inheriting that capability as a managed service and reaching the market in a fraction of the time — the same centralised-platform logic that has repeatedly proven faster and cheaper across open banking deployments.

What institutions need in place to participate in the cVRP scheme

As one of the organisations named in the UK Payments Initiative, obconnect sees the same readiness checklist come up for every bank and PSP weighing cVRP:

- Scheme participation — alignment to the UKPI rulebook, standards and conformance, without negotiating bank by bank.

- PISP / ASPSP connectivity — reliable, FAPI-aligned API connections to initiate and service payments across the market.

- Consent and mandate management — capturing, storing and enforcing long-lived VRP mandates and their parameters, with a clean audit trail.

- Name and account verification — Confirmation of Payee and account checks to keep mandate setup secure and reduce misdirection and fraud.

- Resilience and reporting — always-on infrastructure and the management information a regulated scheme demands.

obconnect provides this as centralised, managed infrastructure, so institutions can participate in the scheme and bring cVRP products to market by connecting to a proven platform rather than building and maintaining their own.

The window is now

The UK has spent over fifteen years without a new major payment scheme. cVRP changes that, and Wave 1 is the moment to act — before e-commerce arrives and the institutions that moved early own the head start. The technology question is settled. The only question left is whether to build on the scheme yourself, or connect to it.

Talk to obconnect about building on the cVRP scheme

cVRP is a payment scheme — the shared rules, standards, participant obligations and commercial arrangements, operated through the UK Payments Initiative. It is not a product itself; banks and fintechs build recurring-payment products (such as a “Pay by Bank Monthly” option) on top of it, just as products are built on Visa, Bacs or Faster Payments.

Commercial Variable Recurring Payments is a UK payment scheme for recurring account-to-account payments. It lets a customer authorise a long-lived, parameter-bound mandate so products built on the scheme can collect variable payments over Faster Payments — a consent-driven alternative to Direct Debit and card-on-file.

UKPI is the new, industry-owned body that operates the cVRP scheme, launched on 2 June 2026 — the UK’s first new major scheme since Faster Payments in 2008. Funded by 31 founding organisations, it provides the single rulebook, standards and shared commercial model so firms don’t have to negotiate bank by bank.

Wave 1 went live on 2 June 2026, covering regulated and trusted sectors. Wave 2, for general e-commerce, is expected in the second half of 2026.

Institutions either build their own scheme-compliant PISP/ASPSP capability or connect through an existing UKPI participant that operates the infrastructure as a managed service — covering scheme participation, connectivity, consent management and verification.